Privacy Policy

At Drawback Hero, your privacy is a top priority. This Privacy Policy explains how we collect, use, disclose and protect your personal information when you visit our website or use our services.

1. Information We Collect

We collect various types of information to provide and improve our services, including:

a. Personal Information

- Name, email address, phone number and business details.

- Payment and billing information (e.g. bank account details for duty refunds).

b. Non-Personal Information

- Browser type, IP address and other technical data.

- Website usage data collected through cookies and similar technologies.

c. Client Data

If you submit data related to refund claims, such as shipping documentation and transaction records, we store and process this information securely.

2. How We Use Your Information

We use your information to:

- Process and file duty refund claims on your behalf.

- Provide account management and client support.

- Improve website functionality and service offerings.

- Communicate updates, promotions or service notifications.

- Comply with legal obligations.

3. How We Share Your Information

We do not sell or rent your personal information. However, we may share it with:

- Service Providers: Third parties that assist us in providing services (e.g. payment processors, cloud services).

- Business Partners: Trusted partners to facilitate certain features or integrations.

- Legal Authorities: If required by law or to protect our legal rights.

4. Data Security

We implement technical and organizational measures to protect your data against unauthorized access, alteration, disclosure or destruction.

However, no method of transmission over the internet is 100% secure. We encourage you to take precautions to protect your account.

5. Your Rights and Choices

Depending on your location, you may have the following rights:

- Access and Correction: Request access to or correction of your personal data.

- Data Portability: Request a copy of your data in a portable format.

- Deletion: Request that we delete your personal data, subject to legal and contractual obligations.

- Opt-Out: Unsubscribe from marketing communications at any time.

To exercise these rights, please contact us at [INSERT CONTACT EMAIL].

6. Cookies and Tracking Technologies

We use cookies to enhance your experience on our website. You can manage your cookie preferences through your browser settings.

7. International Data Transfers

If you are located outside of Canada or the United States, your data may be transferred to and processed in countries where data protection laws may differ from your home jurisdiction.

8. Third-Party Links

Our website may contain links to third-party websites. We are not responsible for the privacy practices or content of those sites. We encourage you to review their privacy policies.

9. Children's Privacy

Our services are not intended for individuals under the age of 18. We do not knowingly collect personal information from children.

10. Changes to This Privacy Policy

We may update this Privacy Policy from time to time to reflect changes in our services or legal obligations. We will notify you of significant changes through our website or by email.

11. Contact Us

If you have any questions about this Privacy Policy or our data practices, please contact us at [INSERT CONTACT EMAIL].

Questions about your data?

Our team is happy to walk you through how we handle and protect your information.

Contact Us →Canadian Customs & Trade Compliance Resource

Canadian Types of Duty Drawback: A Complete Guide

Understanding the Canadian types of duty drawback is essential for businesses that import goods into Canada and later export, manufacture, return, or destroy them.

This guide explains every category available under Canadian customs regulations.

The Main Canadian Types of Duty Drawback

Exported Goods Drawback

Refunds available when imported goods are exported in the same condition. This is one of the most common Canadian types of duty drawback.

Manufacturing Drawback

Duties paid on imported inputs may be refunded when used in goods manufactured in Canada and exported.

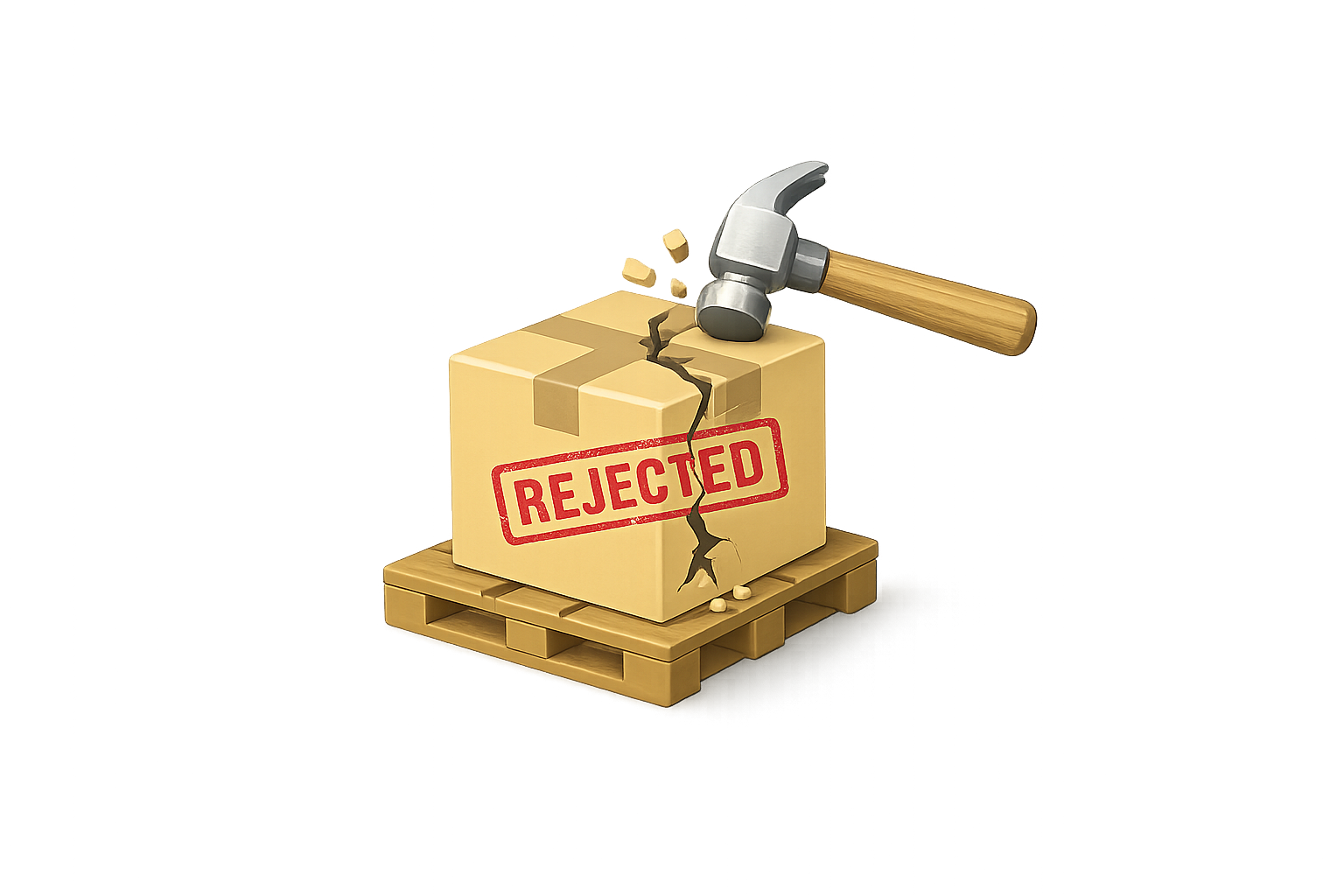

Rejected Goods Drawback

Available when imported goods are returned to suppliers due to defects or non-compliance.

Destroyed Goods Drawback

Duties may be recovered when goods are destroyed under CBSA supervision.

Substitution Drawback

In some cases, equivalent goods may qualify under substitution provisions.

NAFTA/CUSMA Restrictions

Certain exports to the U.S. or Mexico are subject to drawback limitations.

Exported Goods Drawback

Exported Goods Drawback is the most commonly used category among the Canadian types of duty drawback.

This applies when imported goods are exported in the same condition in which they were imported. If the goods were not used, altered, or substantially transformed before export, duties paid at the time of import may be refundable.

Who It Applies To

Distributors importing finished goods for resale abroad

Wholesalers re-exporting excess inventory

Companies shipping goods cross-border to U.S. customers

E-commerce businesses fulfilling international orders

Manufacturing Drawback

Manufacturing Drawback is one of the most strategically valuable Canadian types of duty drawback, particularly for industrial and production-based companies.

What Qualifies:

If you import raw materials, parts, or components and those inputs are incorporated into finished goods exported outside Canada, duties paid on the imported inputs may be recoverable.

Common Industries:

Automotive parts manufacturing

Aerospace and defense

Industrial equipment assembly

Electronics manufacturing

Consumer packaged goods

Rejected Goods Drawback

Not all imported goods meet expectations.

Rejected Goods Drawback applies when imported goods are defective, non-compliant, damaged, or otherwise unsuitable and are returned to the supplier or exported out of Canada.

This is one of the most underutilized Canadian types of duty drawback.

Examples:

Products failing Canadian regulatory inspection

Quality control failures

Incorrect specifications shipped by supplier

Damaged goods discovered post-import

Destroyed Goods Drawback

When imported goods cannot be sold or exported, they may be destroyed. If destruction occurs under CBSA authorization or supervision, duties paid may be refundable.

Destroyed Goods Drawback is highly procedural. Improper destruction or missing documentation can void eligibility.

This applies to:

Expired products

Damaged inventory

Safety recall items

Non-compliant imports

Substitution Drawback

Substitution Drawback allows for refund claims when identical or commercially interchangeable goods are substituted in export scenarios.

This is more technical and applies in specific regulatory circumstances where inventory commingling occurs.

It is less common but can be highly valuable for high-volume operations managing standardized goods.

Because substitution rules are complex, professional review is recommended.

NAFTA/CUSMA Restrictions

Certain exports to the United States or Mexico may be subject to drawback limitations under the Canada–United States–Mexico Agreement (CUSMA).

Companies exporting to the U.S. or Mexico should review drawback eligibility carefully to ensure compliance.

Under CUSMA rules:

Drawback may be limited to the lesser of duties paid in Canada or duties paid in the importing country

Specific calculations may apply

Duty Drawback Expertise for Canadian Businesses

We specialize in helping Canadian importers, exporters, and manufacturers navigate the Canadian types of duty drawback under the Customs Act and CBSA regulations.

With in-depth knowledge of documentation requirements, eligibility criteria, and regulatory compliance, we assist businesses in preparing accurate and compliant drawback claims.

Specialized focus on Canadian customs drawback

Understanding of CBSA audit standards

Structured documentation review process

Experience across multiple industries

Frequently Asked Questions

What is duty drawback in simple words?

Duty drawback is a refund of customs duties paid on imported goods that are later exported, destroyed, or used to produce goods that are exported. If the goods don’t remain in the country for domestic consumption, the duties paid may be recoverable.

How does duty drawback work?

A company imports goods and pays customs duties. If those goods are later exported or otherwise qualify under drawback rules, the company can file a claim with customs authorities to recover eligible duties.

Who is eligible for duty drawback?

Importers, exporters, manufacturers, and distributors may qualify, provided they can document that imported goods were exported, incorporated into exported products, returned to suppliers, or destroyed in accordance with regulations.

How do I know if I qualify for duty drawback?

Goods may qualify if they are:

- Exported in the same condition

- Used in manufacturing exported products

- Returned to a supplier

- Destroyed under customs supervision

Specific eligibility requirements vary between the U.S. and Canada.

How is duty drawback calculated?

Duty drawback is generally calculated based on the amount of customs duties originally paid on the imported goods. In some cases, trade agreements or destination country rules may affect the refundable amount.

Do I really pay nothing upfront?

Correct. Drawback Hero works on a contingency fee basis. We invest our time and expertise to identify, prepare, and file your claims. Our fee is a percentage of the refund we recover. If we don't recover anything, you owe us nothing. There are no retainers, setup fees, or hourly charges.

SOCIALS

CONTACT US

TYPES OF DRAWBACK

LEGAL

Copyright 2026. All Rights Reserved.